Taxes on selling land in Michigan include a 4.25% state capital gains tax plus federal taxes ranging from 0-20%, but strategic planning can significantly reduce your tax burden. Michigan's relatively low state rate and available deductions make it more favorable than many states. Understanding timing strategies, step-up basis benefits, and proper documentation can save you thousands.

Key Takeaways

- Michigan charges a flat 4.25% capital gains tax on land sales, which is lower than many other states.

- Step-up basis rules for inherited land can eliminate most or all capital gains taxes when selling property you inherited.

- Proper timing and documentation of improvements can significantly reduce your taxable gain through legitimate deductions and strategic sale timing.

Quick Note: If you're looking to skip the traditional sales process and sell Michigan land fast, we can provide a free, no-obligation cash offer within 48 hours.

Understanding Taxes on Selling Land in Michigan

When you're considering a land sale in Michigan, understanding the tax on selling land is crucial for making informed decisions. Michigan landowners face both federal and state tax obligations that can significantly impact their final proceeds from the sale.

Michigan's Tax Landscape for Land Sales

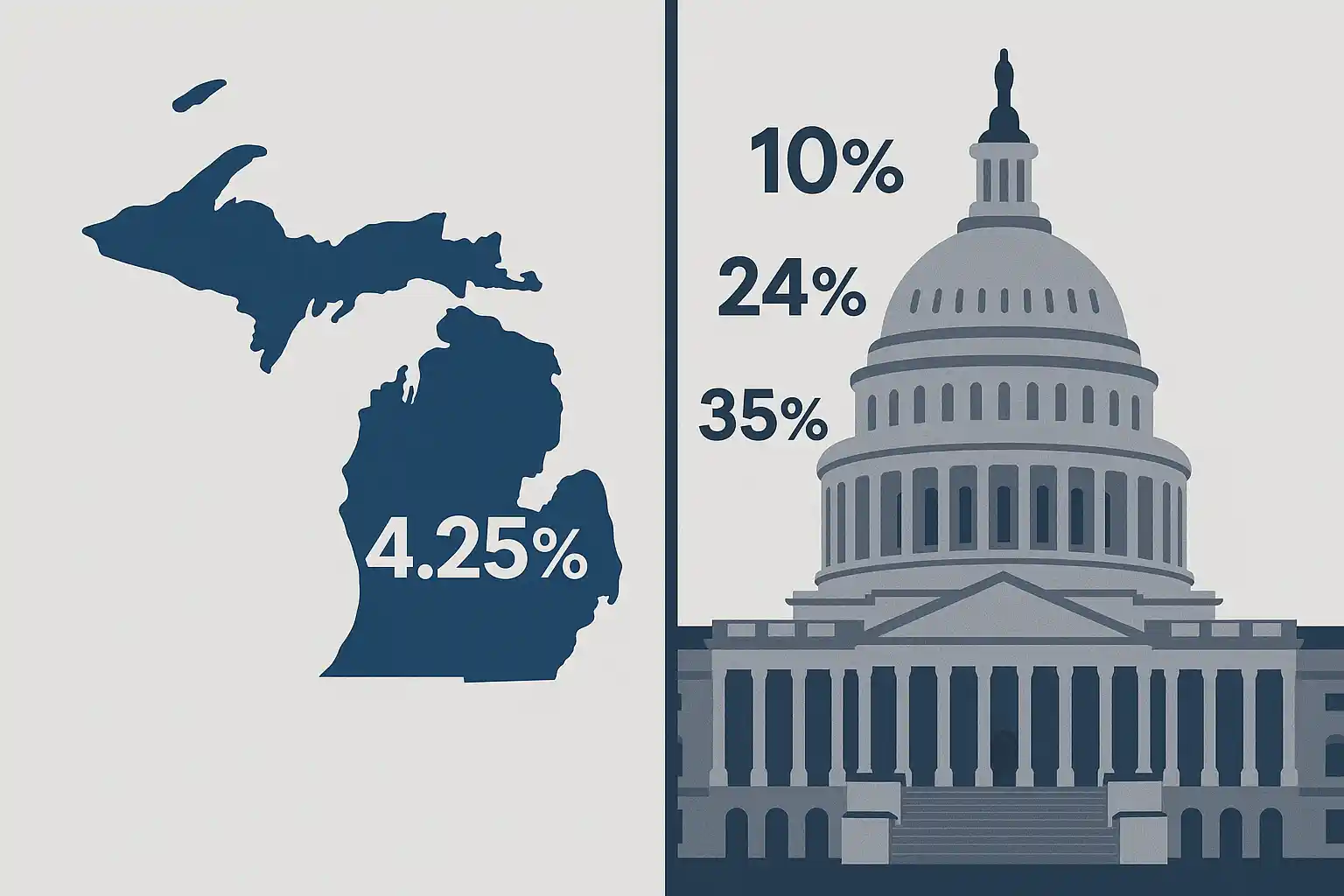

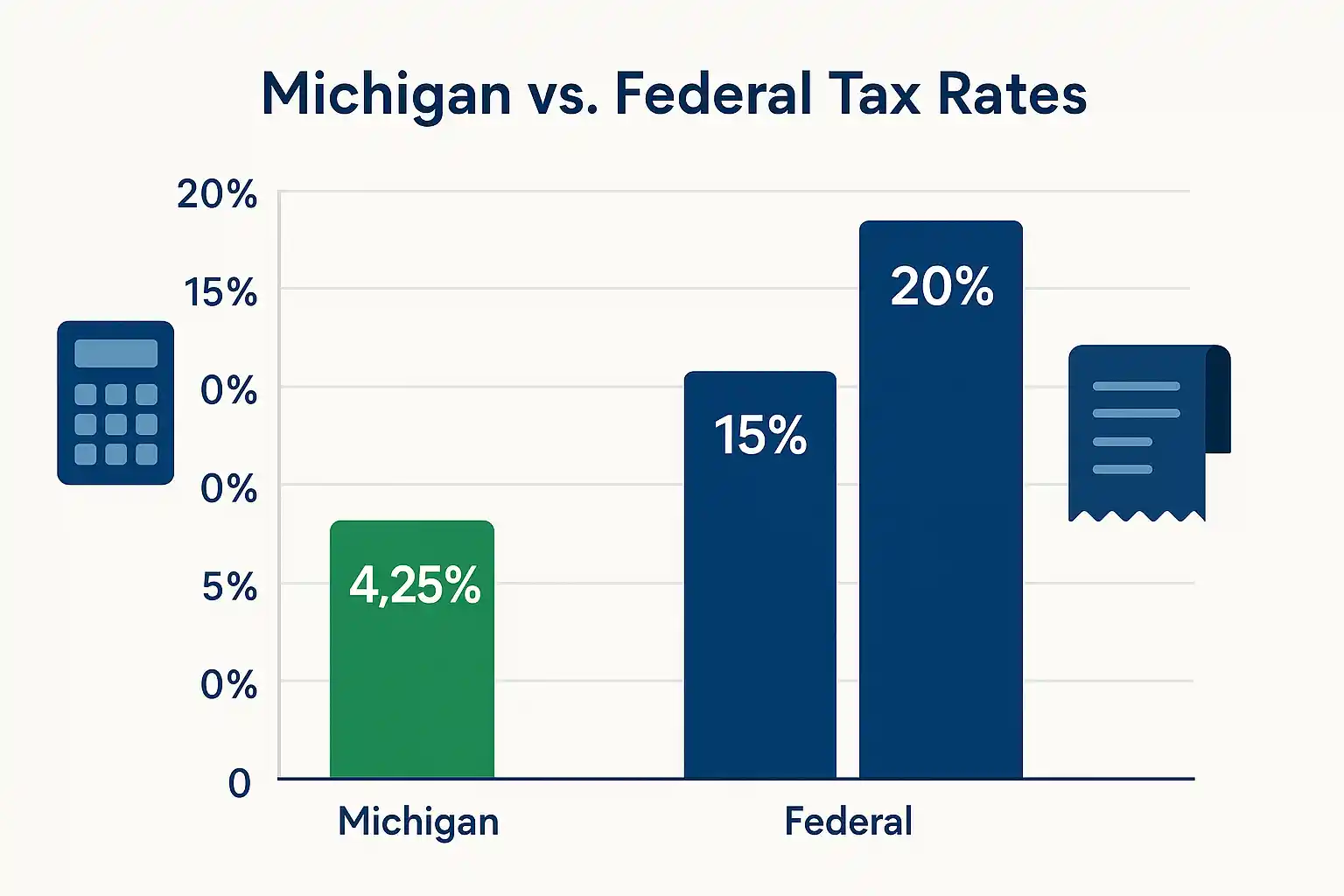

Michigan treats capital gains from land sales as regular income, taxed at the state's flat rate of 4.25%. This relatively modest rate makes Michigan more favorable compared to many other states. However, you'll also face federal capital gains taxes, which range from 0% to 20% depending on your income level and how long you owned the property.

Types of Taxable Land Transactions

Taxes on selling land in Michigan apply to various scenarios:

- Vacant land sales - Raw acreage, buildable lots, or undeveloped property

- Investment property - Land explicitly purchased for resale profit

- Inherited property - May qualify for favorable step-up basis treatment

- Business property - Commercial or agricultural land used in trade

Federal vs. State Tax Considerations

The complexity of land sale taxation involves multiple layers:

- Short-term gains (owned less than one year) - Taxed as ordinary income

- Long-term gains (owned over one year) - Preferential federal rates apply

- Depreciation recapture - If you've claimed depreciation on improvements

- Net Investment Income Tax - Additional 3.8% federal tax for high earners

When Professional Help Makes Sense

Many landowners ask, "If I sell my land, is it taxable?" The answer depends on various factors, including purchase price, improvements made, and your overall tax situation. Michigan's tax code includes specific deductions for land improvements and selling expenses that can reduce your taxable gain.

For those interested in selling land by FSBO in Michigan, understanding these tax implications becomes even more critical since you won't have a realtor guiding you through the process.

Professional tax consultation is highly recommended for any Michigan land sale, as proper planning can potentially save thousands in taxes while ensuring full compliance with both state and federal requirements.

Is Your Michigan Land Sale Taxable? (What You Need to Know)

Not every land transaction in Michigan triggers a tax obligation, but understanding when taxes on selling land in Michigan apply can save you from costly surprises. The taxability of your land sale depends on several key factors that determine whether you owe state and federal taxes.

Primary Factors That Determine Taxability

The most important consideration is whether you realized a capital gain from the sale. If you sell your Michigan land for more than your adjusted basis (original purchase price plus improvements), you'll typically owe taxes on the profit.

Key taxability triggers include:

- Profit from the sale - Any amount above your cost basis

- Investment property - Land held for rental income or appreciation

- Business use - Property used in trade or business activities

- Depreciation taken - Previous tax deductions that must be "recaptured"

When Michigan Land Sales Aren't Taxable

Several situations can eliminate or reduce your tax liability:

- Sale at a loss - When the selling price is below your cost basis

- Primary residence exclusion - Up to $250,000/$500,000 federal exclusion may apply

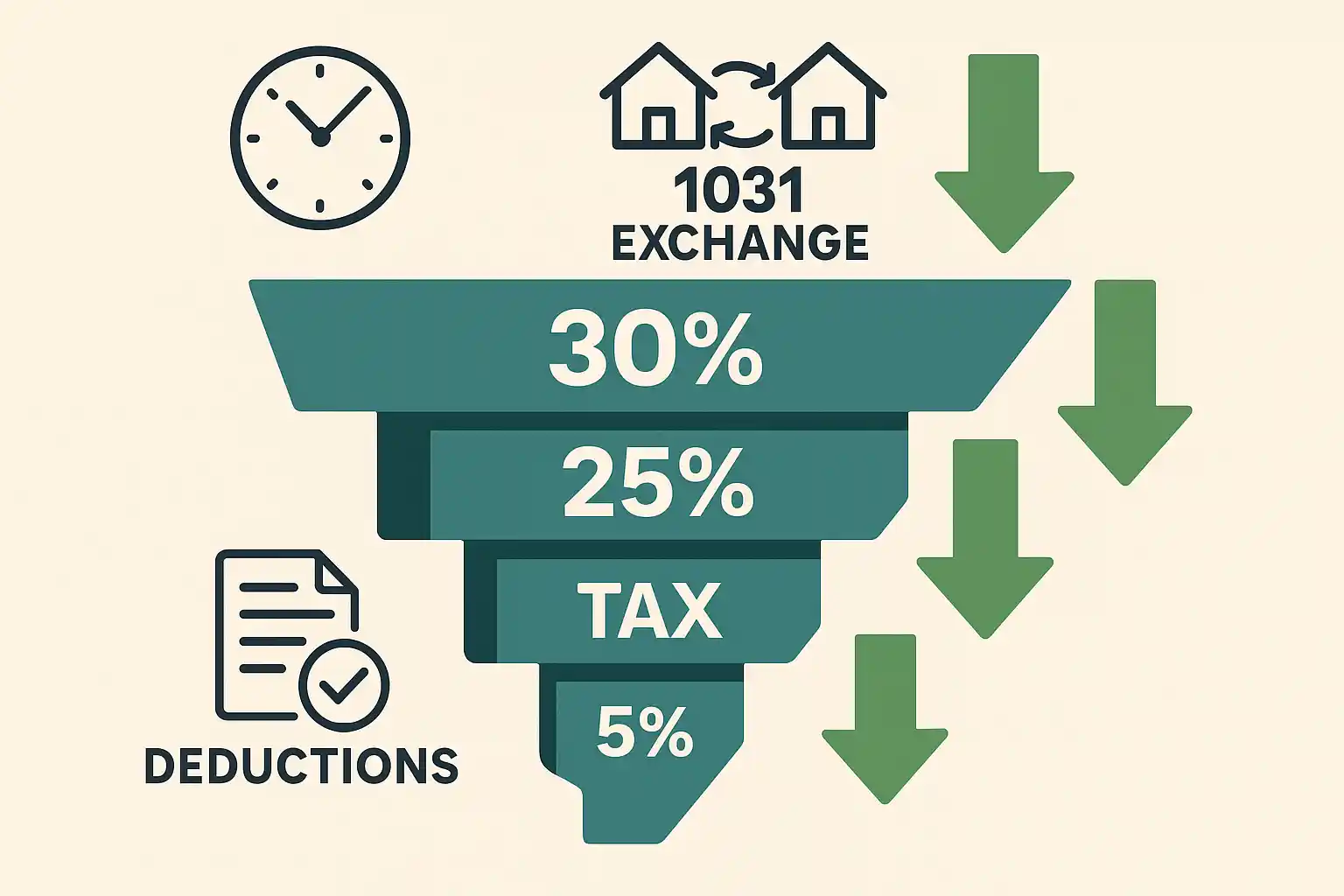

- 1031 exchanges - Deferring taxes by purchasing replacement property

- Installment sales - Spreading gain recognition over multiple years

Special Michigan Considerations

Michigan's tax treatment offers some advantages for landowners. The state's 4.25% capital gains rate applies uniformly regardless of income level, making tax planning more predictable than in many other states.

If you're wondering "if I sell my land is it taxable" in Michigan, remember that even taxable sales may have significant deductions available for:

- Selling expenses - Real estate commissions, legal fees, marketing costs

- Improvement costs - Survey fees, environmental assessments, infrastructure

- Holding costs - Property taxes paid during the ownership period

Getting Professional Guidance

For those considering how to sell land in Michigan independently, understanding taxability becomes crucial since you won't have professional guidance throughout the process.

How to Minimize Capital Gains Tax When Selling Michigan Land

Learning how to avoid capital gains tax when selling land in Michigan requires strategic planning and understanding of available tax reduction methods. While you can't eliminate taxes on profitable land sales, several legitimate strategies can significantly reduce your tax burden.

Timing Your Sale Strategically

The timing of your Michigan land sale can dramatically impact your tax liability:

- Hold for over one year - Qualify for long-term capital gains rates (0%, 15%, or 20%) instead of ordinary income rates

- Coordinate with income timing - Sell in lower-income years to stay in favorable tax brackets

- End-of-year planning - Time sales to optimize overall tax situation

- Harvest tax losses - Offset gains with losses from other investments

Maximize Your Cost Basis

Your taxable gain equals the sale price minus your adjusted basis. Increasing your basis through legitimate expenses reduces taxable income:

- Document all improvements - Wells, septic systems, clearing, grading, surveys

- Track holding costs - Property taxes, insurance, maintenance expenses

- Legal and professional fees - Attorney fees, appraisals, environmental studies

- Marketing expenses - Advertising, signage, real estate photography

Advanced Tax Strategies

Michigan landowners have several sophisticated options for minimizing capital gains tax:

1031 Like-Kind Exchanges:

- Defer all capital gains by purchasing replacement investment property

- Must identify replacement property within 45 days

- Complete exchange within 180 days

- Properties must be of "like-kind" (investment or business use)

Installment Sales:

- Spread the gain recognition over multiple years

- Receive payments over time instead of a lump sum

- Helpful in staying in lower tax brackets annually

Documentation and Compliance

Proper record-keeping is essential for maximizing deductions and ensuring compliance. Understanding the paperwork needed to sell land in Michigan helps ensure you don't miss valuable deductions.

Michigan Tax Rates and Deductions for Land Sales

Understanding the specific tax rates and deductions available for Michigan land sales can help you accurately estimate your tax liability and maximize your after-tax proceeds. Michigan's tax structure includes both state and federal components, plus transfer taxes that vary by county.

Michigan State Tax Rates

Michigan applies a flat 4.25% tax rate to all capital gains, including land sales. This straightforward approach makes tax planning more predictable compared to states with graduated capital gains rates.

Michigan tax structure includes:

- Capital gains tax: 4.25% on all gains regardless of income level

- No preferential rates: Long-term and short-term gains taxed equally at state level

- Standard deduction: Available to reduce overall taxable income

- Consistent application: Same rate applies to all types of real estate sales

Federal Tax Rates for Land Sales

Federal capital gains rates depend on your income and how long you owned the property:

Long-term capital gains (held over 1 year):

- 0% rate: For single filers earning up to $47,025 (2025)

- 15% rate: For income between $47,026 and $518,900

- 20% rate: For income above $518,900

- Additional 3.8%: Net Investment Income Tax for high earners

Short-term gains (held less than 1 year) are taxed as ordinary income at rates up to 37%.

Michigan Transfer Tax Structure

Transfer taxes are separate from income taxes and are due at closing:

State transfer tax: $3.75 per $500 of sale price ($7.50 per $1,000)

County transfer taxes vary:

- Kent County: Additional local fees may apply

- Ottawa County: $8.60 per $1,000 total rate

- Ingham County: $0.55 per $500 county rate

Available Deductions and Expenses

Michigan allows deductions for legitimate selling expenses and improvements:

- Real estate commissions: Full deduction for broker fees

- Legal and closing costs: Attorney fees, title insurance, escrow

- Property improvements: Surveys, environmental assessments, infrastructure

- Marketing expenses: Advertising, signage, professional photography

- Professional services: Appraisals, tax consultation, accounting fees

Proper documentation is essential for claiming all available deductions and ensuring compliance with Michigan tax requirements.

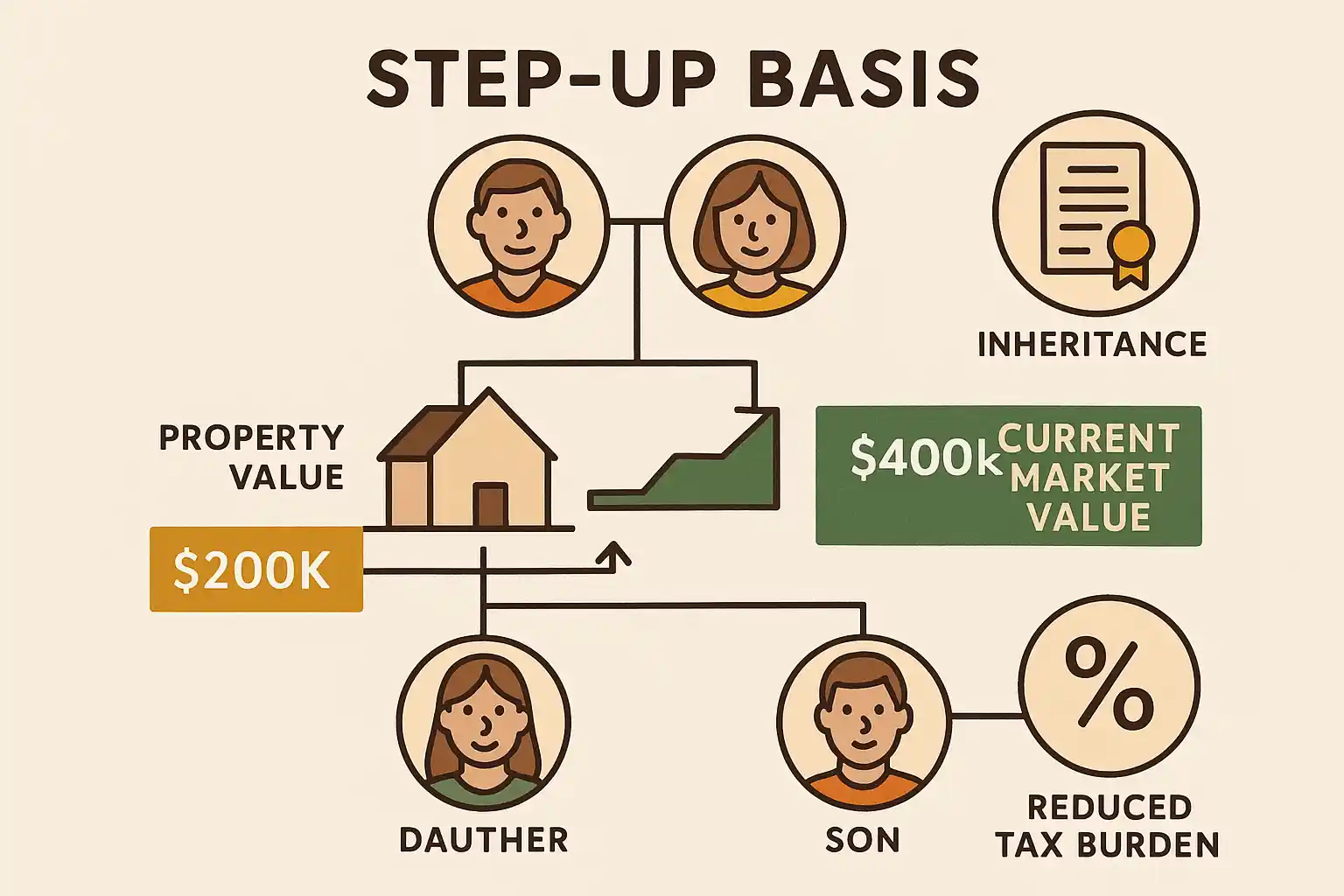

Tax Benefits of Inherited Land Sales in Michigan (Step-Up Basis)

Inheriting land in Michigan comes with significant tax advantages that can dramatically reduce or eliminate capital gains taxes when you sell. The step-up basis rule is one of the most valuable tax benefits available to heirs, potentially saving thousands in taxes compared to gifted property.

Understanding Step-Up Basis

When you inherit Michigan land, the IRS "steps up" your cost basis to the property's fair market value on the date of the original owner's death. This means you start with a clean slate for tax purposes.

Key step-up basis benefits:

- Eliminates built-in gains - No tax on appreciation that occurred before inheritance

- Reduces future capital gains - Your basis equals the current market value

- Applies to all inherited property - Raw land, improved property, investment real estate

- Available for joint ownership - Surviving spouses may receive a full step-up in community property states

Inherited Land vs. Gifted Land

The tax difference between inherited and gifted land is substantial:

Inherited property advantages:

- Step-up basis to current fair market value

- No capital gains on pre-death appreciation

- Simplified record keeping - Fresh start for tax basis calculations

Gifted property disadvantages:

- Carryover basis - Inherits the original owner's low basis

- Immediate tax liability on all appreciation since the original purchase

- Complex documentation requirements for accurate basis calculation

Michigan-Specific Inheritance Considerations

Michigan follows federal inheritance tax rules, but has its property transfer requirements:

- No Michigan inheritance tax - The State eliminated inheritance taxes

- Property transfer affidavits are required for proper basis documentation

- Probate proceedings may be necessary for a clear title transfer

- Multiple heirs may require partition or buyout arrangements

Maximizing Inherited Land Tax Benefits

For those considering selling inherited land in Michigan, timing and documentation are crucial:

Essential steps include:

- Obtain a professional appraisal as of the date of death for the basis of establishment

- Maintain inheritance documentation - Will, probate records, death certificate

- Consider timing - Immediate sale often results in minimal taxable gain

- Evaluate improvements - Any enhancements after inheritance increase the basis further

Professional tax consultation is essential when selling inherited Michigan land to ensure you receive all available tax benefits and comply with both federal and state requirements.

Simplify Your Michigan Land Sale Taxes with Cash Buyers

Navigating Michigan land sale taxes can be complex, but working with experienced cash buyers streamlines both the sale process and tax reporting requirements. Professional land buyers understand Michigan's tax landscape and can help optimize your transaction for better tax outcomes.

Why Cash Sales Simplify Tax Reporting

Tax documentation advantages:

- Clear purchase contracts - Simplified 1099-S reporting

- Fast closing timeline - Better control over tax year timing

- No financing contingencies - Eliminates deal uncertainty

- Professional guidance - Experienced buyers understand tax implications

Timing Benefits for Tax Planning

Cash transactions offer flexibility that traditional sales cannot match:

- Choose your closing date - Optimize for current or future tax year

- Quick turnaround - Complete sales within 2-3 weeks

- Avoid carrying costs - No extended marketing periods increase holding expenses

- Immediate liquidity - Cash in hand for other tax planning strategies

Expert Support Through the Process

When you work with professional land buyers, you get guidance on Michigan-specific tax considerations and documentation requirements. This expertise helps ensure proper compliance while maximizing your after-tax proceeds.

Ready to simplify your Michigan land sale? We buy Michigan land fast, typically providing cash offers within 24-48 hours.

Get your free cash offer today - no obligations, no fees, just straightforward tax-optimized land transactions.